Are you thinking about financial freedom, owning your own home, or taking that big trip you’ve always wanted? You don’t need stock market expertise or a large budget to get started. Even small amounts like €50 a month can grow into real wealth over time. The key is to start early. Today, see how it works, which investment options are worth considering, and what to keep in mind to start growing your money with confidence!

In a nutshell:

- Build an emergency fund first: ideally, 3 months’ worth of income before starting to invest

- Your investment strategy should be based on your goals and time horizon. Short-term savings are not the same as investing

- Spread your money across different types of investments to reduce risk

- Products like Go & Grow can be one option to start with, with up to 6%* p.a. returns and near-instant access*

- Review your portfolio regularly and adjust as your life evolves

Why should beginners start investing?

Saving alone isn’t enough anymore. Inflation reduces the purchasing power of money sitting in your bank account. By starting to invest early, you protect your savings, benefit from the power of compounding, and steadily build wealth step by step.

This brings you closer to your goals, whether it’s preparing for retirement or enjoying more financial freedom. The best part: You don’t even need deep financial knowledge or a big budget to start with!

✅ Stay ahead of inflation: Savings accounts rarely beat inflation. Investing gives your money the chance to grow in the long run.

✅ Compounding is your friend: Returns on previous returns can add up over time. The earlier you start, the more your money can do for you.

✅ Reach your goals faster: Whether it’s a dream vacation or your first home, investing gets you there step by step.

✅ It’s easy to get started: With simple-to-use products like Go & Grow, you can start from as little as €1.

✅ Start building long-term financial independence: The sooner you start, the more freedom you’ll have later in life.

Join over 500,000 investors

Yes, that’s what you earn with Go & Grow. Daily payouts. Near instant access – no lock-up period.

Is it worth investing small amounts?

You don’t need thousands to begin! Many people start with just €50 per month. For beginners, building the habit matters more.

Example:

You invest €100 monthly at Go & Grow for 10 years, with up to 6%* per year in returns. After 10 years, that could grow up to €16,000 thanks to the compounding effect!

The table below shows how regular investing could grow over time with an annual return of 6%:

| Monthly investment | 5 years | 10 years | 20 years | 25 years | 30 years |

| €50 | €3,489 | €8,194 | €23,102 | €34,650 | €50,226 |

| €100 | €6,977 | €16,388 | €46,204 | €69,299 | €100,452 |

| €250 | €17,443 | €40,970 | €115,510 | €173,248 | €251,129 |

| €500 | €34,885 | €81,940 | €231,020 | €346,497 | €502,258 |

Want to see for yourself? Use the calculator on our website!

Beginners investing: How does it actually work?

Your investment plan should fit your life. There is no one-size-fits-all approach, but these rules of thumb apply to most people:

- Only invest money you won’t need over the next few years

- Build an emergency fund first

- Even €25 per month is enough to start

- Got a bonus or a gift? One-time investments like €250, €500, €1,000 or €5,000 can go a long way

Investing money for beginners doesn’t have to be complicated. You don’t need a big budget or advanced financial knowledge to get started. What matters is knowing what you are investing for, and how long you can set aside your money. This will help you to find the type of investment that is right for you.

1. Get a clear picture

Start by looking at your financial setup. Ask yourself:

- How much do you spend and earn each month?

- Do you already have emergency savings (ideally about 3 months’ worth of income)?

- How much can or do you want to invest regularly or as a one-off?

Knowing your numbers helps you to invest without financial stress.

2. Define your goals and timeline

Before investing, you should know when you will need your money and what you are saving up for. Are you planning on going on a trip around the world in 3 years or achieving retirement in 30 years? Your goals shape your plan. Considering these questions helps you to define your investment strategy:

- What do you want this money to help you achieve? This could be building wealth for later, buying a house in 5 years, gaining financial independence, or saving up for a retirement fund.

- When will you need it? Short-term savings goals are 1 to 3 years, medium-term goals are 3 to 7 years, and long-term goals start at 7 years or more.

- How flexible will you need to be? If you need to be able to access your funds anytime, your investment strategy will differ from someone who can let their money sit for years or even decades.

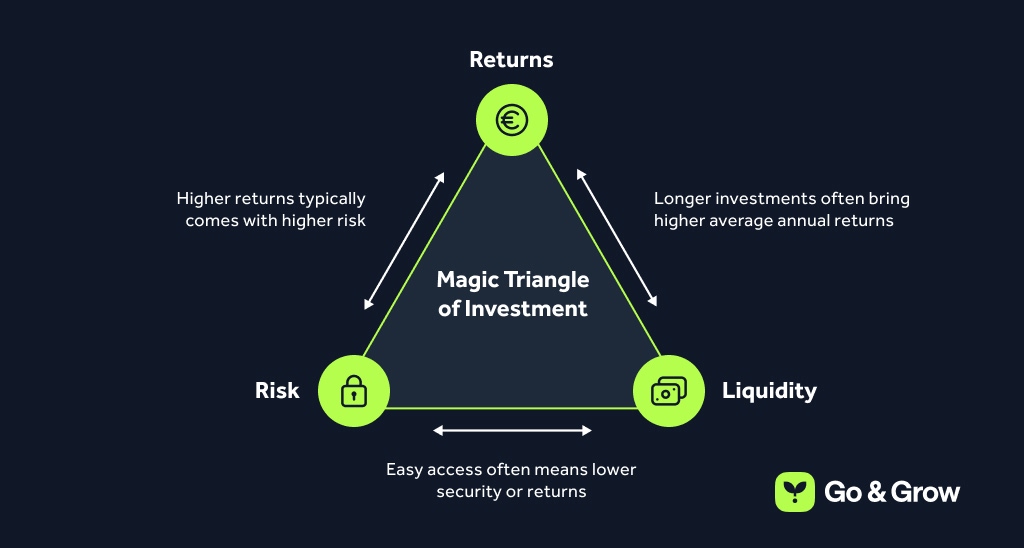

Different answers will lead to different investment strategies. If you want to invest money in the short term, secure and liquid forms of investing will be more suitable.

Would you rather invest for a long period of time? Then you can sit back and relax, even if things take a downturn from time to time. Long-term goals allow you to invest your money at slightly higher risk, thus often gaining higher returns. Time is the biggest advantage when investing money, for beginners and professionals alike!

3. Assess your risk profile

All investing involves some degree of risk. Even “safe” assets like savings accounts can lose value due to inflation, ultimately undermining your wealth-building efforts. The key is determining which level of risk aligns with your goals.

To find your “sweet spot,” consider your investment horizon and run through different market scenarios: How would you react if your portfolio dropped by 20% overnight? Generally, high-risk investments offer greater potential returns but require more active involvement and a higher stress tolerance to navigate market volatility.

- Low risk, conservative: Your main focus is to preserve your capital with as little fluctuation as possible. This category includes, for example, savings accounts, bonds, and conservative funds.

- Balanced: If you are willing to take moderate risks, investments in ETFs, mixed funds, or managed brokerage accounts can be suitable.

- Risk-aware: The focus here is on investments with the highest returns. To this end, investments can be made in, e.g., stocks, cryptocurrencies, or thematic funds.

Tip: Don’t start by chasing high returns. Begin with an investment form that lets you sleep at night. As you gain experience, you can gradually add products with more ups and downs to your portfolio.

4. Emergency fund: security over returns

Before you start investing, set aside a financial buffer you can fall back on in an emergency.

- This money is intended for unexpected expenses, not investments

- These can include repairs, job loss, or long illness

- If something unexpected happens, you can fall back on this fund instead of taking out expensive loans

It’s a good idea to keep about 3 months’ worth of income set aside and easy to access. What matters most is being able to reach this money quickly and hassle-free in an emergency, without losses or waiting times.

Investing for beginners: Investment options compared

There is a wide range of opportunities offered to beginners and experts to invest their money. Not every type of investment fits every person or point in life, though. Every type has its own pros and cons, depending on goals, risk profile, and timeframe.

When investing money as a beginner, it is worth taking a look at the most common options. Once you understand how they work, you can decide which combination suits you best.

| Investment Option | Volatility | Flexibility | Annual Return | Best For |

| Go & Grow | Stable historical performance, returns may vary | Near-instant access | Up to 6%* | ✅ Competitive returns |

| Fixed deposit (up to 12 months) | Very low | Locked in | Ca. 1.77%¹ | ❌ Too inflexible |

| P2P loans | Medium to high | Sometimes daily access | Ca. 5-17%2 | ⚠️ Use trusted platforms only |

| Money market funds | Low to medium | Typically accessible in 1-2 days | 1.5-2.2%3 | ⚠️ More complex, limited real-return potential |

| Short-term government bonds | Low (varies by issuer) | Traded daily | Ca. 1.96%4 | ❌ Market-specific |

| ETFs | High | Traded daily | Ca. 7%5 | ❌ Better for long-term investing |

| Stocks | Very High | Traded daily | Depends | ⚠️ For experienced investors |

| Crypto | Extremely volatile | Tradable 24/7 | Depends | ❌ Very speculative |

Join over 500,000 investors

Yes, that’s what you earn with Go & Grow. Daily payouts. Near instant access – no lock-up period.

How to start an investment: Building your first portfolio

Investors don’t have to pick just one option. Spreading your money across different types of investments (diversification) helps balance risk and return.

One possible approach is to combine ETFs with products like Go & Grow, depending on your goals and time horizon. This way, you can start small, keep your portfolio well-balanced, and build a possible foundation with little to no administrative effort.

Here’s an example portfolio:

| Focus | Investment Type | Goal |

| Cashflow & Flexibility | Go & Grow | Daily returns, near-instant access, high diversification |

| Long-term growth | ETFs | Higher returns long-term with market movement |

| Emergency account (optional) | Current account, savings account | For last-resort emergencies |

1. Solid foundation & up to 6%* returns per year: how does Go & Grow work?

Go & Grow is a European-based product where you can invest in consumer loans. Investors earn daily returns on their balance, up to 6%* per year. Everything runs automatically, with your money being available near instantly.*

Here’s how the business model works:

- You add money to your Go & Grow account, starting from just €1

- Your money is automatically spread across thousands of small loan fractions (diversification to reduce risk)

- Bondora issues consumer loans to customers in several EU countries, with the most important markets being Finland, Denmark, the Baltics, and the Netherlands

- You earn daily returns on your account, up to 6%* per year

- No lock-ins, you can withdraw your money anytime!*

Good to know: You don’t lend to individuals, but invest in a broadly diversified pool of loan fractions.

Over 500,000 investors have joined Bondora and Go & Grow since 2008. Active investors have collectively invested more than €2 billion and earned €179 million in returns.

Aleks’ Testimonial provided directly to Go & Grow

“I’ve been with Go & Grow for more than 6 years and have been very satisfied. It’s easy, consistent, and I can withdraw my money anytime.* Go & Grow is my go-to investment, even in uncertain times.”

2. Solid addition: What are ETFs?

ETFs (Exchange Traded Funds) are investment funds traded on the stock market that track an index, such as the S&P 500 or MSCI World. By investing in an ETF, you automatically spread your money across many different companies. This lowers risk and saves time.

Why beginners like ETFs:

- Broad diversification: lower risk by investing in many companies

- Low fees

- Flexible to buy and sell

- Easy to automate with a savings plan, for example, starting from €25 a month

Final tips: How to invest as a beginner

Investment for beginners can be overwhelming, but a few basic rules help you find the path to financial independence much more relaxed. Here are a few tips for everyone new on board:

1. Saving is not investing

Savings means setting money aside for, e.g., repairs or unforeseen expenses. Investing, on the other hand, aims to build up capital in the long run, taking more risks but earning higher returns, too. Both have their place; what’s important is striking the right balance.

2. Starting small is better than not starting at all

You don’t need a large sum to get started. Some investments can be made with as little as €1 per month! The important part is to start as early as possible to fully take advantage of compound interest effects. Experience is better than perfection.

3. Don’t speculate on shortcuts and quick profits

Investing is not gambling! Those who rely on “hot tips” or short-term trends risk losses. Solid investing is founded on patience, discipline, and long-term planning.

4. Automation helps you stay on track

Regular investing via standing orders or automated platforms ensures you can build capital without much effort. It works automatically and without the constant pressure to make decisions.

5. Think long-term

It is normal for markets to move or prices to fall. Selling in panic is one of the most common mistakes made by beginners. However, temporary price slumps are part and parcel of ETFs and stocks in particular. Those who stick to their strategy and invest for the long-term, or focus on investments without price fluctuations, can remain relaxed even in the event of a stock market crash.

Keep reviewing and adjusting

Your investments should grow with you. Major changes, such as a job change, moving house, or starting a family, can also influence how much you can or want to invest.

You shouldn’t constantly change everything, but rather regularly check whether your current strategy still suits your own circumstances:

- Life changes: A career change, starting a family, moving abroad, or a major purchase can affect how much and how often you can invest. In such cases, it makes sense to review your monthly contributions or temporarily pause them. Many products, such as Go & Grow, offer flexibility as needed.

- Reassess your investment goals: Have you achieved your original goal (e.g., building up a nest egg)? If so, the next step may be to reallocate your money to higher-yielding investments.

- Rebalancing: Those who invest in different asset classes often observe a shift in their ratio over time due to price developments. Rebalancing allows you to restore these ratios to equilibrium, for example, once a year.

Especially with investments for beginners, you don’t want to have to deal with financial details all the time. Investments, such as Go & Grow, which offer automation and diversification, can be especially helpful here.

Join over 500,000 investors

Yes, that’s what you earn with Go & Grow. Daily payouts. Near instant access – no lock-up period.

The bottom line: Building capital? Just start

Investing money for beginners isn’t difficult. If you start early, invest regularly, and keep a cool head, you can achieve a lot over time, even with small amounts. You don’t need a lot of up-front capital or in-depth financial knowledge, but above all, patience and clarity.

Before you invest, you should:

✅ Build an emergency fund

✅ Get an overview of your income, expenses, and debts

✅ Know your goals, timeframe, and risk profile

It’s important to think long-term and spread your money across different types of investments. Each option comes with its own mix of opportunities and risks, from diversified choices like Go & Grow to more volatile options such as ETFs.

By investing consistently and adjusting your investments from time to time, you can build up your assets in a structured way, even without any prior knowledge.

FAQ – Investing money for beginners

How do you start investing money?

Start by reviewing your finances and building an emergency fund (about three months’ income). Then set your goals and timeline, and choose a suitable product, such as an investment account or an ETF savings plan.

What is the best way to invest money?

The best way is the one that fits your life. For most beginners, a long-term, diversified approach works well, for example, regular deposits into an automated platform. The key is to stay consistent and avoid reactive decision-making over market swings.

What is the best investment for 10 years?

ETFs or other long-term products are well-suited for a 10-year horizon. If you’re open to more risk, digital investment accounts can be a good addition. Focus on low fees, broad diversification, and a steady plan. Traditional savings accounts won’t deliver much over this period.

How to invest money for beginners?

Begin with an emergency buffer. After that, invest small amounts regularly, ideally on autopilot. Many platforms manage the details for you, so you can stay focused on your goals.

1 Average bank deposit rates for savings in the EU (Oct 2025)

2 Average rates for P2P platform returns (Nov 2025)

3 Average returns for money market funds (Nov 2025)

4 Returns for short-term bonds in the Eurozone (Nov 2025)

5 Average S&P 500 annual return over the long term (Nov 2025)

{kind=link}